So how do we deal with the 2016 risk environment?

I'm an old timer at this game...30 years and counting so I favor playing the odds and not sticking my neck out too far on long shots. That means sticking to what works...delta neutral pairs (or three's) and trading the momentum/mean reversion paradigm shifts in the major indices where the rampant market maker and HFT price manipulation tends to be constrained.

Going forward we'll look at some possibilities that we can turn into probabilities using the paradigm models and/or a delta neutral tactic when the signals are unaligned.

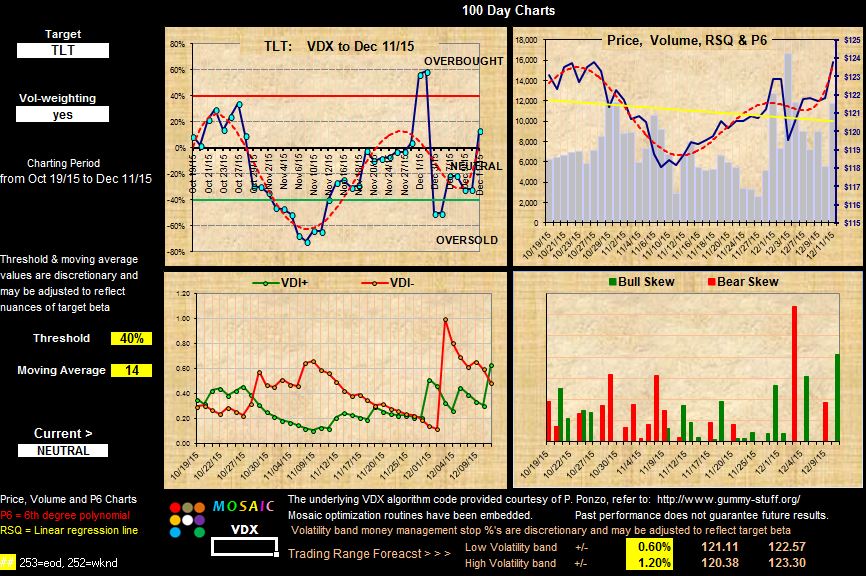

Today's focus...bonds in the form of I-Shares 20 year treasuries ..TLT and its 2x short inverse TBT.

We'll also include our typical neutral outlier XLU (SPYDR Sector Utilities).

Since TBT is a double inverse we have to double the stop setting to achieve risk parity.

Here's the 2 year snapshot of this setup and below that the stop calculation panels. Note that the stop panels are all downslope RSQ and P6 reflecting a lower VIX and tighter trading ranges. This dramatically affects our current stop settings.....and our risk exposure. 45 days ago calculated settings were TLT .7 and TBT 1.4 and the odds are we'll see those parameters again (maybe soon).

Click on charts to enlarge.