Our long VXX signal captured a nice 1/5% gain at the close while in after hours trading VXX was up another .75%. A number of significant technical breakdowns are apparent across multiple sectors and the current odds favor more near term consolidated downside action Expect another major short covering rally but beware the subsequent Trap Door setup that's likely to follow.

For now the volatility signals are proving more reliable than the equity signals so that's where our dollars are currently deployed....along with a sizable risk on position in silver (SLV).....with current signal metrics to be posted later this week as time permits.

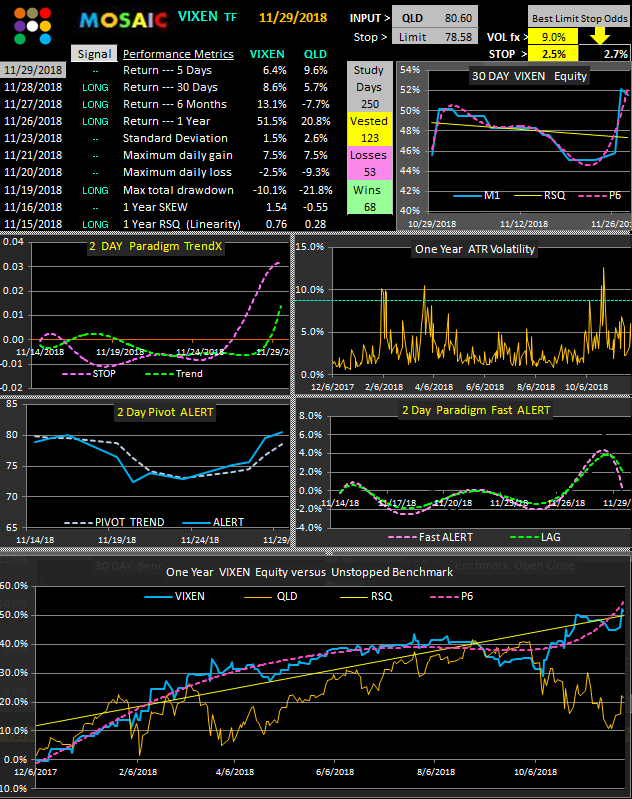

A reasonable trader looking at the VXX win/loss ratio would likely say..."Well. that looks terrible"

However, the magic of this trading model is hidden in the strict adherence to the specified limit stop and the willingness to accept limited losses while also accepting big winners.

The linearity of the equity curve of the Vixen versus VXX tells the real story.

Keep in mind that out of 250 trading days (1 year) the model was only vested 119 days, slightly less than 50% of the time.

Also keep in mind that VXX has a built in decay function due to it futures composition so betting on any long VXX position is akin to paddling upstream. That's not an excuse for the win/loss ratio, just a extenuating factor that further muddies the water when trying to trade VXX.