Today was the first posting of the new M3 / M3R models. Yes there are no performance improvements and the RSQ, P6 and associated equity curves look different (improved) from the previous version. This is part of M3's evolution and refinement and adaptive nature.

I trade this model daily for multiple accounts and other family members do as well so I have a vested interest in making M3 a success. Long time Mosaic followers know that I'm very risk adverse and always follow a mantra of capital preservation. The new M3 models embody these goals.

It may be surprising, but most of the model performance improvement derives from an in depth analysis of alternate stops and the decision to go forward with the simple 2 and 1.5 % limit stops.

These stops are wider than the previous ATR calculated stops but it turns out that giving the model "room to breathe" during daily volatility swings actually pays off handsomely in the end.

The other variable is in the rankings and the desire to decrease "lag" or the delay in moving out of a waning momentum position and into a rising momentum position. The new M3 momentum algorithm has been very modestly accelerated...in fact over the rolling backtest of 120 trading days (2 years lookback) the average number of accelerated position rankings was 4, slightly more than 3%.

Again, it was the decision to adopt a wider stop spread than really added juice to the returns.

As stated in the M3 disclaimer all posted stops are strictly for the purposes of establishing performance benchmarks. I'm not a financial adviser and you alone are responsible for when and if you decide to pull the trading trigger. Any stops posted as well as any rankings are strictly for the purposes of discussion and education. Each trader can, and is encouraged to, develop their own risk management program according to his or her personal risk tolerance. M3 is simply a reflection of what I' doing on a day to day basis. I've discussed the various types of stops in a previous post and the limit stop is what I prefer and what is utilized in calculating the performance metrics of the models.

A very wise trader once told me "Anybody can get into a trade, it's when you exit that determines how successful you are". I've learned the painful truth of that statement over several decades.

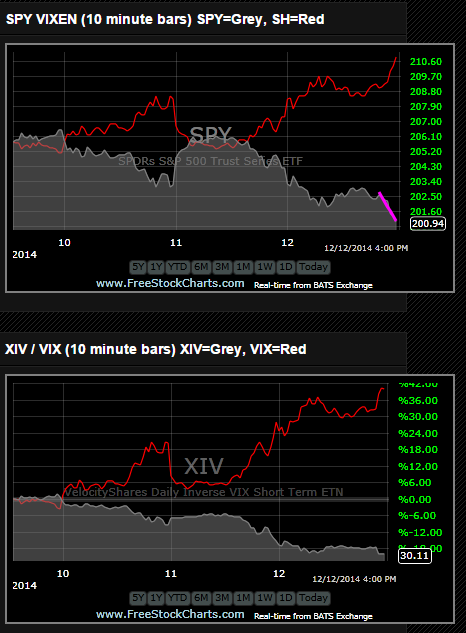

Note that both M3 and M3R look at 6 inputs on a daily basis but only the top 3 are displayed.

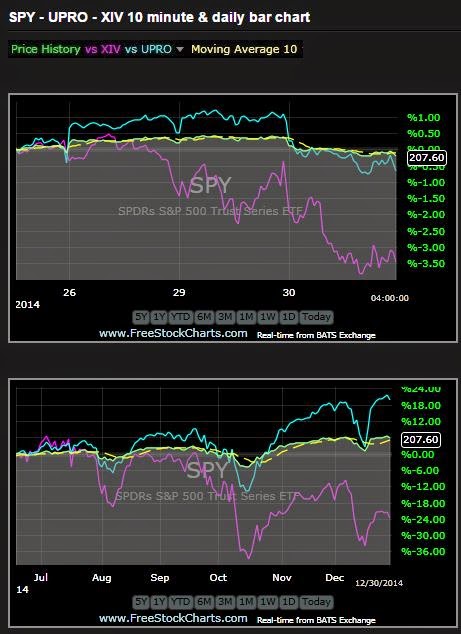

Here then are the recent 6 month equity charts for M3 and M3R>>>>>