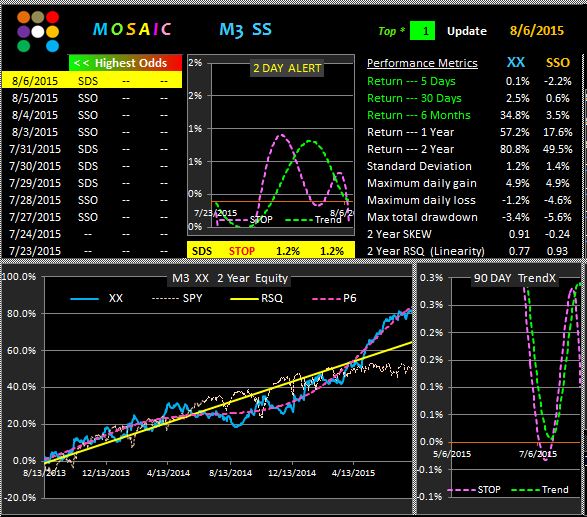

There's apparently some confusion about the SSO/SDS model posted last week.

Here are the rules in a nutshell:

1. Each day at the close have equal dollar amounts of both SSO and SDS.

2. Place a 1.2 % limit stop on each position

3. Return at the end of the next day and repeat step 1 if one of the positions has been stopped out. That's it.

Our goal is a steady income stream with very little drawdown.

We use a market neutral ,smart beta tactic to accomplish our goal.

We use the 2x leveraged SPY ETFs to increase beta and hence our potential return.

The model makes money whenever daily volatility exceeds a defined "normal level", which actually varies over time as the mean of VIX fluctuates.

Today the model generated 1.2% gain on the SSO side = .6% based on total capital at risk.

A lot of days nothing happens because the volatility range doesn't trigger the stops.

On those occasions we just sit tight and wait of the next day.

It's the strategically placed stops that make this model work.