I'll delay the MRSI and DB studies for a couple days to deal with a recent query:

Several readers have asked whether this might be a good time to sell covered calls on the LM and TAQK models.

Covered calls are typically used as a means to lock in recent portfolio gains and with that strategy in mind certain criteria should be observed:

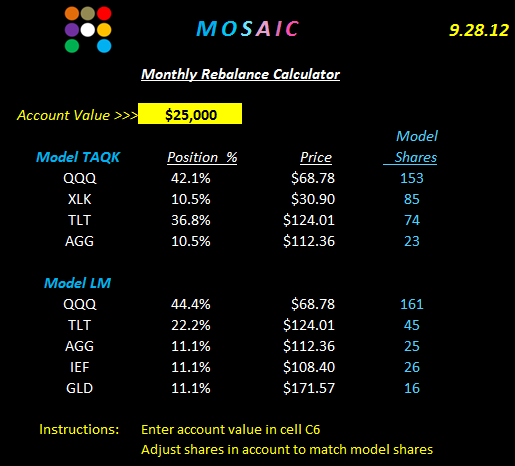

The LM ETFs are QQQ, TLT, AGG, IEF and GLD.

The TAQK model includes XLK, QQQ, TLT and AGG.

AGG has virtually no option volume so there's little opportunity there.

IEF has very thin volume and the spread tends to widens as volume contracts so we need to be careful with that one. A slightly out of the money 1 month call is $.35 or about .32% premium..a trivial amount,a slightly in the money call is $ .90 or .8% premium.

QQQ has active volume, narrow spreads and huge open interest. A 1 month slightly out of the money call is $ .81 or 1.2% premium, a slightly in the money call is $ 1.41 or 2% premium.

TLT also has active volume and narrow spreads. A 1 month slightly out of the money call is $ 1.50 or 1.2%, a slightly in the money call is $ 1.97 or 1.6%.

GLD also has active volume and narrow spreads. A 1 month slightly out of the money call is $ 2.39 or 1.4%, a slightly in the money call is $ 3.35 or 1.95%.

XLK (TAQK model.. has thin volume and open interest. A 1 month slightly out of the money call is $ .15 or .3%, a slightly in the money call is $ .64 or 2%.

Now, the tricky part becomes one of betting which way the market is going next. If you think that equities are overbought and due for a pullback then selling the QQQ calls and or XLK calls are a great idea.

If you think the markets will run higher then selling TLT calls is the way to go.

GLD has been on a run for a while and is currently at levels seen a year ago, just before the retracement kicked in. Selling calls on the GLD position will lock in some of those recent gains and still allow GLD to climb a couple bucks without compromising the total return of the investment.

We've just got to keep in mind that LM and TAQK are market neutral models, designed to offset volatility by playing equities against bonds with a few wild cards like GLD in the mix. What we don't want to happen is to have short call positions exercised and called away thereby exposing the portfolio to higher volaility (and drawdown) because one side of the balance equation has been eliminated.

So how do you deal with that risk?

One solution is that when most of the premium has been squeezed out of a position, simply close the position, book the gains and then reopen a new ETF position in the proper percentage allocation (and possibly sell calls against the new position).

The down side to this tactic is that it can end up looking like a dog chasing its tail and may incur a number of commission costs..

There are other tactical option strategies to offset the risk of exercise but they are beyond the scope of the current post.