In the case of Mosaic M3 we track 3 distinct paradigms >>

MR, a mean reversion model, which basically buys the 3 day low.

MN, a momentum model, which basically buys the 3 day high.

SS, a market neutral model, which uses SPY leveraged ETNs to capture above average volatility.

I say "basically" for MR and MN because there are embedded algorithms in each model that filter for linearity and correlation of the ranking calculations. In times of extreme volatility the models will retreat to cash.

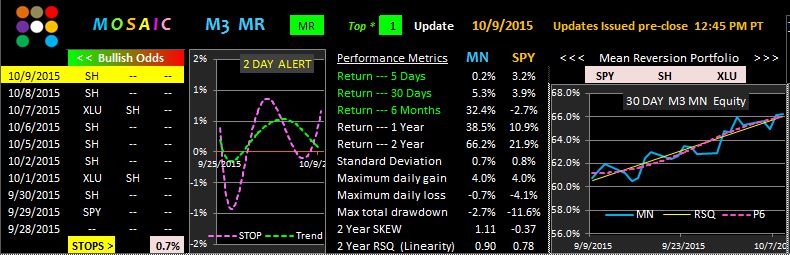

Given the inherent drivers for MN and MR we would expect MN, the momentum based model, to do well in strongly trending markets, whereas MR will perform better in a stepping type of market environment or in a consolidation market.

We can detect the current paradigm (and focus our capital accordingly) by examining the performance metrics and the equity curves of each model.

In the versions of MN and MR shown the returns are based on the top 1 ranked positions.

On the daily updates we use a version of MN using the top 2 ranked inputs as our goal is to minimize

portfolio flux and help identify when changes in paradigm are most likely.

Based on a cursory exam of the 2 equity curves we are currently in a trending market. This is confirmed by the MR model which indicates extreme weakness in SH (SPY inverse) and no ranking for XLU, whose appearance in the rankings should provide an early warning for a pending paradigm shift.