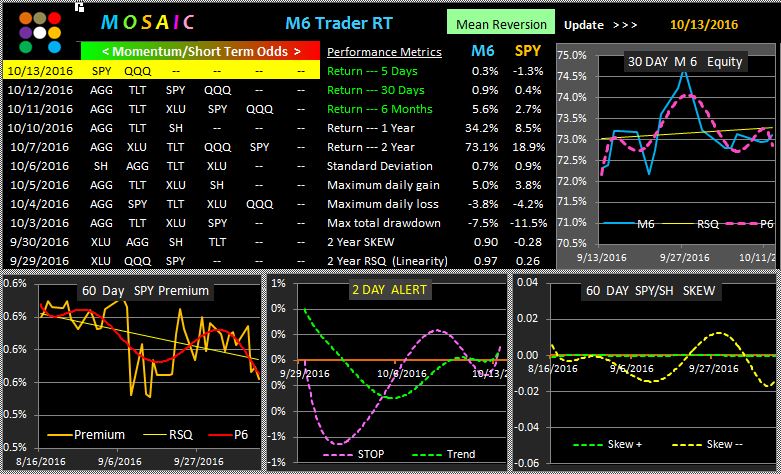

The trick of course is in maintaining a diversified long/short beta portfolio. One striking difference between the models is the longer term trend of the #1 ranked positions (eg, AGG) in the me4an reversion model versus the more volatile status of #1 ranked positions in the momentum model.

My own personal preference is for the mean reversion mode since it tends to produce the most reliable signals even at the expense of lower total returns. Just my opinion...not investment advice.