The RM versions of the Mosaic models have gone back to cash as of today's open. We're seeing more whipsaw action in the RM models than in the previous 4 year lookback. Clearly there's instability in the markets and the upcoming earnings season will likely only accentuate that volatility.

Today's studies explore 2 sectors that one would normally expect to show superior results relative to our wide sector default model. First, the tech sector where we look at some of the high fliers along with QQQ. Just for risk exposure purposes analysis we'll use AGG as our baseline.

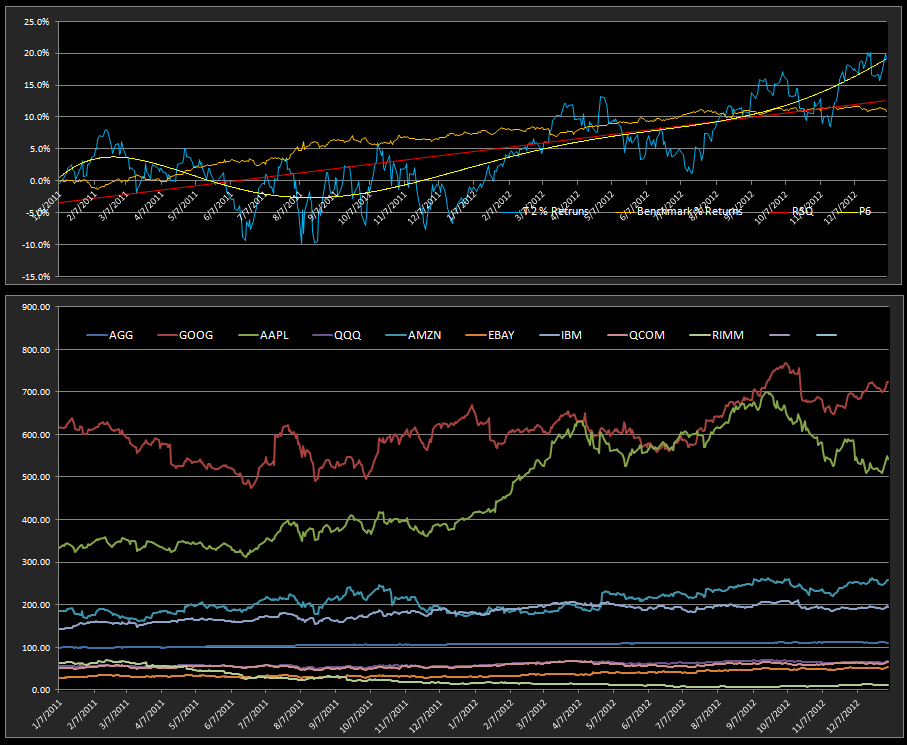

What's interesting is that when we choose the top 2 or the top 9 the results are pretty much the same. Looking at the 2 year charts of the components below allows us to see the volatility profile a bit clearer. It also makes clear the need for stops when looking at the RSQ and P6 curve.

Then we look at the gaming sector (which also includes resorts and cruise lines (RCL and CCL).

Again we have used AGG for the baseline. And, in contrast to the all bond portfolio profiled last week the volatility on this portfolio is an attention getter. You can play with top 1,2,3,4 etc models but it doesn't get better. The 2 year component charts are shown below displaying a bumpy ride along the RSQ equity line.

This is a clear case where the risk is not worth the reward. As we saw last week...there's much easier ways to achieve a 10-11% APR with much, much less risk.