Note that the Momentum rankings should now be adjusted on Monday's Open rather than Friday's close.

This decision is based on a recent look at how the markets have performed between Friday's Open and Monday's Close and it reflects a small edge that can be achieved by trading Monday's Open...which actually has been consistently lower than Friday's close during our lookback period.

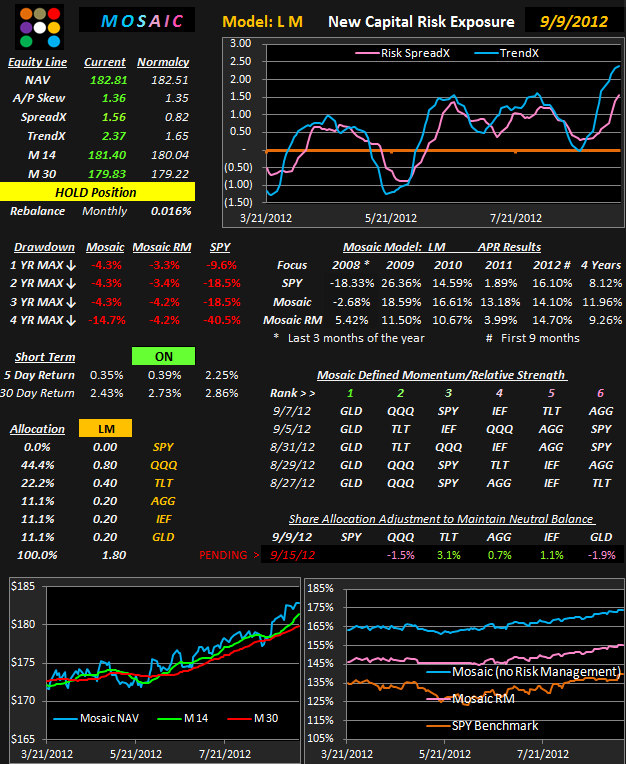

TIP has been replaced by IEF in the T 3 component mix. WHY?. Because now all the Lazy Man components are reflected to the T3 mix and there's no need to replicate (and confuse) readers with multiple views of the same data. That applies to the Situations version of the Lazy Man where all 6 components are held in equal dollar amounts and it also applies to the allocation version of Mosaic (shown below) that holds varying % of the capital account in each of the 6 components.